Regulations in lending: The Equal Credit Opportunity Act (2/7)

UCL Letter #6: April 20, 2020

Welcome to the sixth letter of Undirected Cyclic Thoughts. The last letter served as the first of seven posts in a series on lending regulations. It outlined the Truth in Lending Act, one of the earliest laws still relevant to this day. Today we’ll focus on the second regulation to be examined: The Equal Credit Opportunity Act.

If you are not one of the dozen people who subscribe to this newsletter, the context for this series can be found at the top of the first post: Regulations in lending: TILA (1/7).

If you are one of the dozen people who subscribe to this newsletter, sorry for the delay - I know this is the highlight of your quarantine and that you’ve put your life on hold for the past 20 days to hear what comes next. For better or worse, I’m trying to launch something by end of quarantine and, as always, my estimates for shipping were a bit, erm, optimistic.

So. Let’s get to it!

The Equal Credit Opportunity Act

This is the second act mentioned in Synchrony’s list of lending-laws-that-we-may-or-may-not-be-breaking. Unlike the TILA, the Equal Credit Opportunity Act (or ECOA as we’ll be referring to it) does not receive a special shoutout explaining exactly why it concerns the firm. But, fear not! Once you force yourself through the next 4000 words, you will very quickly understand what risk it poses.

Note to reader: This is a good time to close this tab, feel a small twinge of guilt but quickly move on with your life.

Note to reader: If you’re still reading this, I’m sorry for you. I hope Netflix comes out with something new soon.

Ok, so similarly to what we did with the Truth in Lending Act, the best way to understand the ECOA is to look at the decade or so leading up to its introduction. The ECOA was first enacted in 1974. I say first because it took our lovely Congress a few tries to get it right… reminds me of a certain ally’s killsquad performance in 2018. Anyway, this means we’re looking at the 60s for clues as to how we got the ECOA. Luckily, you don’t have to look very hard.

Wait? All men are created equal?

If you try to summarize the 60s in one sentence and neglect the Civil Rights Movement, you should really go back to grade school… or move out of Mississippi. One of the two.

The 60s was the decade of the Civil Rights Movement and set the stage for the ECOA.

The Civil Rights Act of 1964 banned discrimination based on “race, color, religion, sex or national origin” in employment practices and public spaces.

The Fair Housing Act of 1968, which was the most filibustered piece of legislation in our nation’s history, expanded prohibitions on discrimination to include the sale, rental and financing of housing.

The majority of the nation was up in arms demanding equal rights, demanding that all men (and women) are treated equally, and pushing for change in many aspects of society.

And although one could read various civil rights acts as applying to discrimination in finance and lending, the banks clearly didn’t. The only explicit call-out to date was discrimination based on race, religion, and national origin was prohibited in the sale, rental and financing of housing. Meaning discrimination continued in other departments of our nation’s banks. Not only that, but the Fair Housing Act itself left some protected classes out to dry, including those on federal income support and those without a Y chromosome.

As with many social issues, change often comes from (1) injustice and (2) enough people caring about that injustice. Luckily, the preceding few decades in the U.S. meant just about every household cared about injustice as it pertained to lending.

One nation, Under debt, Indivisible…

In the previous letter we discussed the explosion of credit in the 50s. We looked at a nation obsessed with three things: homeownership, auto ownership, and grease in your hair. The 60s were no different (minus maybe the grease?).

Between 1945 and 1967, consumer credit skyrocketed in the U.S. In 1945, there was $7B in consumer credit outstanding, or about $50 per person. By 1967, that number was $100B, or about $500(!) per person.

Despite a change in the order of magnitude of outstanding debt, the processes behind lending weren’t progressing at the same speed. Loan officers were often making lending decisions based off dubious “algorithms.” There wasn’t much in the way of automated credit scoring. Lenders were using hard copies of credit reports as well as additional “facts”. “Facts” such as, and I kid you not, a person’s reputation. THEIR REPUTATION!

I mean, if you confronted a loan officer in the 60s and questioned their “algorithm,” it’s not like they’d have nothing to show. They’d definitely show you their fancy scorecard. Scorecard? Yes, scorecard. Back in the day, loan officers used scorecards to determine creditworthiness. They’d get a list of factors and they would score each by their very standardized and unbiased intuition.

Unfortunately, this didn’t work out well for a lot of Americans, including white people! As late as the early 70s, lenders were routinely requiring single, widowed, or divorced women to provide a male relative as a cosigner. Not only that, they were discounting the wage of working women even if they were the primary breadwinners. I mean, Jesus, discounting an already discounted wage… freedom and equality for all, huh?

Congress: We should do something

In the early 70s, Congress started kicking around a bunch of bills designed to clean up discrimination in lending. By late 1974, Congress had gotten one through the Senate and signed into law by President Ford. The ECOA was one of a series of lending-related acts and was formed as an amendment to a consumer protection act passed in the late 60s.

The act itself was quite brief - much more digestible than the TILA. It set out a pretty basic purpose: insure that credit is made available with fairness, impartiality and without discrimination on the basis of sex or marital status. Wait, what was that again? “[…] without discrimination on the basis of sex or marital status.”

Sadly, the one bill that made it out to the senate floor was one that seemed to forget about the whole Civil Rights Movement of the decade prior. The laws may have had changed a good bit since the early 60s but the composition of the legislature hadn’t. And it showed.

Prohibited Discrimination

The amendment itself prohibited discrimination in two ways:

(a) It shall be unlawful for any creditor to discriminate against any applicant on the basis of sex or marital status with respect to any aspect of a credit transaction.

The last part of that sentence is important: “with respect to any aspect of a credit transaction.” This would later be interpreted to include aspects as removed as bank locations and language-specific ads.

(b) An inquiry of marital status shall not constitute discrimination for purposes of this title if such inquiry is for the purpose of ascertaining the creditor's rights and remedies applicable to the particular extension of credit, and not to discriminate in a determination of creditworthiness.

This is a not-very-important carve-out of the above and not worth spending too much time on.

Definition of Credit

Unlike the TILA which went to great lengths to define various forms of credit - revolving and non-revolving, floating vs. fixed interest - the ECOA made it quite simple.

It’s credit if it is affording a debtor that right to (a) differ payment of debt, (b) incur debt, or (c) purchase property or services and pay later.

Regulations

The ECOA carved out a set of regulations to accompany the act, however, they were not set by Congress. Instead, Congress put in a placeholder to keep everyone happy. “We’ll get to this after enactment but before the effective date.” In hindsight, this probably wasn’t a great idea, as the very exercise of aligning on the regulations sent Congress back to the drawing board to right their wrongs.

Overriding the States

Nonetheless, they did have the wherewithal to say, “we don’t know exactly what the regulations will be, but we take precedence over whatever <insert state name, default=Alabama> is telling their residents.”

If you’re familiar with this period of U.S. history, you’ll be well aware that Congress had good reason:

With that in mind, the ECOA made it clear that this act overrides state laws with minimal exceptions. Moreover, it explicitly called out a few instances where state laws are no longer valid:

Any state law that prevents separate extension of credit to each spouse does not apply when each spouse voluntarily applies for separate credit from the same creditor.

Should each spouse apply and obtain credit accounts with the same creditor, their accounts cannot be aggregated or combined for determining charges or loan ceilings.

If you don’t take the carrot, here’s the stick

Lastly, they laid out the penalties. Should lenders choose to ignore this law, as their governors ignored civil rights acts for quite some time, they would face consequences.

There are three parts to the punishment here, and they seem to bite.

Damages to Applicant: If you do not comply with a requirement, you owe the aggrieved applicant the sum of the damages sustained by the applicant.

Punitive to Applicant: If you do not comply with a requirement, you may owe the aggrieved applicant up to $10,000 in punitive damages.

Punitive in Class Action: The total recovery of a class action lawsuit shall not exceed the lesser of $100,00 or 1% of the net worth of the creditor.

Where were you last decade?

In April 1975, the Board of the Fed met to align on the regulations which would accompany the ECOA. At this proceeding, the first set of regulations were proposed and commentators were allowed to address the body. Their message, in short, was, “where were you last decade?”

Out of that meeting came two things: (1) an initial set of regulations to accompany the existing Act, and (b) an embarrassed Congress sent out to amend an act passed only 6 months ago.

Regulation B (Unamended)

The initial set of regulations was decent insofar as preventing discrimination based on sex and age. They severely limited the ability to discriminate against a woman, married or not:

A creditor may only require a co-signer if the applicant is not creditworthy

A creditor may not discount the income of an applicant OR an applicant’s spouse because of sex or marital status

A creditor may not ask about childbearing capability or intentions, nor mak assumptions relating to the likelihood of a woman’s leaving the labor force.

Nonetheless, one victory that some did not expect was around credit history. Prior to the ECOA, if a couple had a joint credit line, most of the time information was only reported to the bureaus under the husband’s name. Regulation B nipped that in the bud. Starting after June 1977, creditors were forced to report information in both spouses’ name so long as both spouses either used or were contractually liable for the credit account.

ECOA (Amended)

When Congress came back with its tail between its leg, it seemed to have taken its tongue lashing seriously. In slightly less than a year after the rule-making proceeding of 1975, Congress put forth the Equal Credit Opportunity Act Amendments of 1976.

Within this set of amendments, it first set out to right its wrong with respect to forms of discrimination. It laid out three additional forms of discrimination prevented:

Discrimination on the basis of race, color, religion, national origin, age, sex or marital status

Discrimination based on all or part of an applicant’s income originating from public assistance programs

Discrimination due to the applicant having exercised any right under the Consumer Credit Protection Act (e.g. the parent act of the ECOA)

Next, it added a major new form of protection for all consumers: transparency around applications. Under the amended ECOA, creditors are required to notify an applicant of its action within thirty days of receiving a completed application. Moreover, if the action is adverse (e.g. credit is denied, credit is revoked, an existing agreement is changed), the creditor is required to give a statement of reasons for the adverse action.

This statement of reasons can take two forms: either (i) the reasons spelled out in writing or (ii) a notification that discloses the applicant’s right to a statement of reasons and the identity of the office from which that statement can be obtained.

If you have half a brain, you can imagine that most creditors allotted (and still allot) to go with form (ii). However, this protection was crucial for giving the ECOA any weight at all. Think about it - if you never knew what happened to your application or why it was denied, how could you go about filing a complaint in the first place?! “Excuse me, Mr. DOJ, but I applied for credit and I have a feeling they didn’t like me very much.”

Additionally, the amendments included a raising of the penalties for maximum class action awards from a ceiling of the lessor of $100,000 or 1% of the networth of creditor to the lesser of $500,000 or 1% of the networth of creditor. Why would this matter? Bank consolidation!!! More and more creditors were worth well of $10M, which made an increase to $500,000 or 1% a worthy cause.

To make matters even more serious, the amendment granted the Attorney General authorization to prosecute matters where there is reason to believe a pattern of behavior has occurred.

Lastly, Congress wanted to make sure it got it right this time. As such, it required annual reports on the administration of this act by the Board of the Fed and the Attorney General. These annual reports continue to this day and we’ll dive into few recent ones in a bit.

Regulation B (Amended)

Now by the time the first meeting convened to put together an annual report for Congress, the Fed knew that the original Regulation B was due for some amendments after all the changes to the underlying ECOA. They quickly expanded upon the original to prevent the newly included forms of discrimination, and summarized things into two basic prohibitions:

A creditor cannot discriminate on a prohibited basis, and

A creditor cannot make any oral or written statement to applicants or to prospective applicants that would discourage them, on a prohibited basis, from applying.

They also clarified the adverse action notifications while giving two exceptions to the thirty-day rule:

If the creditor extended a counter-offer, they are given 90 days

If the creditor realized that the submitted application was incomplete and informed the applicant of such, then they do not need to give an adverse action.

All-in-all, by the end of 1976, the ECOA was a pretty good win for the country. The amended act extended to cover most forms of discrimination recognized at the time, and the accompanying Regulation B did a good job of spelling out the details.

Enforcement

With the amended act set to go live in 1977, the FTC, Fed and friends had their work cut out for them. And go to work they did. Over the following decades, they heard complaints, opened investigations, and referred matters that seemed to exhibit a pattern of behavior to the DOJ.

Theories of liability

What resulted from the early DOJ cases was a set of two theories of liability used when prosecuting matters: disparate treatment and disparate impact.

Treatment refers to the process the prospective debtor is subjected to with respect to any aspect of the transaction. Treatment is considered disparate if it is different for an applicant based on a prohibited basis (e.g. race, national origin, marital status). An example of this would be a request for more information from a divorcee vs. a married woman.

Impact refers to the outcome for a prospective debtor. Impact is considered disparate if it results from seemingly neutral policies or practices that have an adverse effect on a member of a protected class and either (i) do not meet a legitimate business need or (ii) whose stated need can be achieved by means less disparate in impact.

An example of disparate impact from policies not meeting a legitimate business need could be higher interest rates blindly charged to Hispanic applicants for auto loans.

An example of disparate impact from policies that can be achieved by means less disparate in impact could be the use of ZIP codes in underwriting. ZIP codes may often lead to discrimination against minority neighborhoods and there are likely better means to calculate individual creditworthiness.

As you can imagine, disparate impact is both the most important and the most difficult theory of liability to unwrap. However, it’s easier to consider by example. To do that, let’s look at these theories of liability in the context of recent reports to Congress.

Reporting to Congress

In September of 2017, the DOJ submitted its annual report to Congress on enforcement activities in 2016. The report gives a good peak behind the curtain of how this act is protecting consumers from discrimination.

Example of disparate treatment

For a case of disparate treatment to be won, it must be shown that the treatment of an applicant of a protected class is materially different than the treatment of a similar applicant of an unprotected class. One example in the report from 2017 is found in United States v. BancorpSouth.

BancorpSouth is a regional bank in the Southeast, but its activities under investigation centered in Memphis. After receiving complaints to the HUD and Bureau, the CFPB sent in undercover operatives to mystery shop credit products. Their finding: the bank failed to provide mortgage lending services on an equal basis to majority African American neighborhoods in the Memphis area.

There were two parts to this allegation: (1) active redlining and (2) discrimination in marketing efforts.

The bank outlined neighborhoods that were primarily African American and then refused to serve them or served them at much higher interest rates. The discriminatory redlining treatment resulted in the bank only opening branches in majority-white neighborhoods and actively discouraging applications from applicants residing in the primarily African American neighborhoods.

Their marketing efforts also fell short. They failed to perform meaningful marketing in the minority neighborhoods. In fact, there was absolutely no specific marketing efforts towards minority communities. Additionally, their advertisements promoted individual loan originators, most of whom were white, failing to market the availability of their product to all creditworthy applicants.

The CFPB consent order required the bank to rectify this through $2.78M in relief to borrowers, $4M in relief to the affected community, and $3M in penalties to the CFPB amongst other requirements.

Example of disparate impact

Now, in order to prove disparate impact, a seemingly neutral policy or practice must be shown to discriminate on a protected basis and either not being necessary for business or its aim be achievable by a means with less disparate impact.

As we discussed previously, this is more complicated than disparate treatment. Under the Trump administration, the CFPB has been under-resourced and enforcement activities under the disparate impact theory of liability have decreased. This has led to most disparate impact cases being focused on auto-lending, where brokers working on behalf of Toyota or Honda have been given too much leeway in setting interest rates. However, we can go back to the Obama administration’s 2013 report for a more nuanced example.

One of the cases mentioned in that report was against Ally Financial (the auto lender owned by GM). The CFPB’s complaint alleged that Ally discriminated by charging over 200,000 non-white borrowers higher interest rater than white borrowers. Although the case was settled, they set out to prove their original allegations by looking at underwriting and pricing results. By using proxies for race, they found that pricing had a disparate impact on minorities despite there not being a credible business need. Had they failed to prove that in court, the CFPB would have been forced to show that there was a similar pricing model that would have a less disparate impact - a feat that has not been proven by the DOJ as of late.

What’s interesting here, is that the CFPB did not need to prove that a certain variable is included, which is responsible for a disparate impact. Instead, they only needed to show that the model in its entirety had a disparate impact. For anyone who’s done a bit of statistics, this poses an obvious problem multi-variate models. With that in mind, let’s look how the 1974/6 ECOA is affecting business today.

What does this mean today?

A lot. In my point of view, the ECOA is a more interesting act than the TILA. The TILA was an attempt at having some sense of law-and-order in a nascent and exploding credit industry. The ECOA was an attempt to make credit opportunities equal, something that is much harder to do. Whereas a business can comply with the TILA by being somewhat organized, a business needs to take a more concerted effort to comply with the ECOA.

Moreover, as both advertising and underwriting have grown much more sophisticated over the past 40 years, businesses are at heightened risks for imposing disparate treatment and disparate impact without malice. Two modern sectors that are clearly seeing these risks are targeted advertising and alternative lenders.

U.S. Government vs. Facebook: Episode 901

It’s no news that Facebook has been in the hot seat with the U.S. government ever since the 2016 election. But, recently the ECOA has played a role in pouring gas on the fire.

Early last year, Facebook settled a series of lawsuits alleging that they were responsible for discrimination as it applied to job, housing and credit advertising. The ACLU, the Communications Workers of America and a few other groups sought to show that by offering micro-targeting features to advertisers (e.g. show an ad to users with children, users in a certain ZIP code, users of a certain age), Facebook was complicit in disparate treatment of protected communities.

According to the plaintiffs, the following use cases were being enabled by Facebook:

If a lender was worried that a handicap person is at a disadvantage in repaying the loan, the lender could exclude users who like pages associated with disabilities (e.g. wheelchair companies, ADA, etc) from seeing their ads.

If a lender was worried that a certain ZIP code represents people who are not creditworthy, the lender could exclude users from those ZIP codes from seeing their ads.

As a result of this settlement, Facebook overhauled their advertising platform. Now, Facebook reviews ads and determines if they belong to a special category. If they are, the advertisers’ microtargeting abilities are severely limited.

Since everything in life is a tradeoff, this meant that running ads in a protected category became much less efficient. Small community banks are now forced to target users who clearly wouldn’t bank with them (e.g. live dozens of miles away) and more and more users see irrelevant ads… (not to equate irrelevant ads and discrimination, but you get the point).

Fintech beware

But Facebook isn’t the only company being affected. In the lending world there’s been a huge push to more sophisticated origination and underwriting practices. Companies like Sofi are using novel datasets and newly-back-in-vogue financial products like income share agreements are taking off.

Nearly all of these startups are trying to gain a competitive advantage through underwriting. The idea is that by using more alternative data (e.g. performance in school, SAT scores, local job market data), lenders can better extend and price credit.

Whereas before someone may have no credit history and be denied financing, now with the help of alternative data a startup may be willing to lend based on projected income due to a STEM degree.

Yet despite these bold and optimistic pitches, the room for error in disparate impact is much larger than before. If you include a seemingly neutral (and maybe even, good) variable in your models, you could very well be denying equally creditworthy minority applicants.

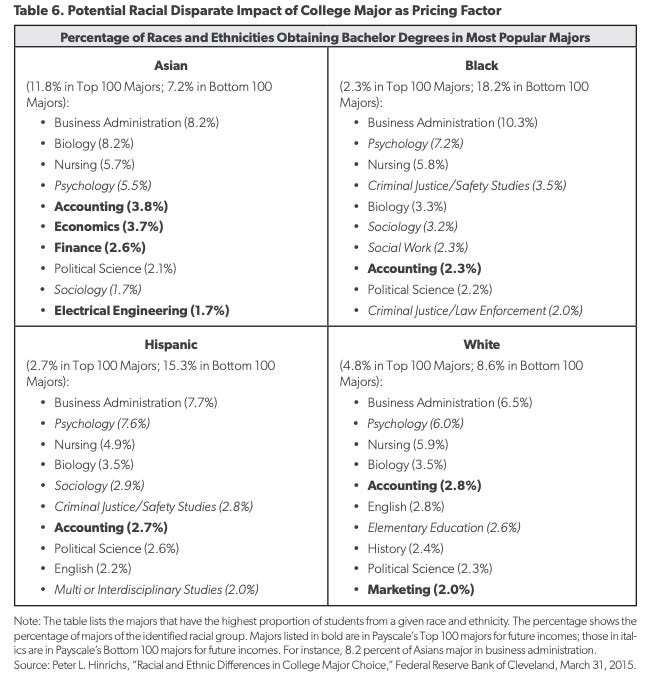

Below is a chart from a study by the AEI, showing that some protected classes would be disparately impacted should a variable like the one we discussed above be weighted highly:

Although no regulation actions have been taken on ISA underwriting or the latest batch of startups offering consumer lending, the courts have already seen relevant drama unfold for traditional lenders.

Sallie Mae Corp, most clearly NOT a startup, used a variable as seemingly innocuous as university-specific default rates in their model for student loans. A decision that wound up costing them a pretty penny after a student sued. The student argued that such a variable unduly penalizes students that attend schools with large minority populations when other, less disparate, variables could have been used. This case was later settled, but I would not be surprised if more come about over the next decade.

Conclusion

Now that we’ve seen how the ECOA originated, the regulation actions taken on its basis, and the concerns it poses for both advertisers and lenders, I think it’s pretty clear what risk Synchrony is referencing in their 10K. They need to keep an eye on their advertising audiences and track as much data as possible to be able to prove both business need and uniqueness of the models, should the CFPB or DOJ come calling.

Although the CFPB may be on uneasy footing under the Trump administration, the takeaway from this post should be that the disparate impact theory is still alive and well and the disparate treatment theory has never been stronger. With that in mind, it’ll be interesting to see how the latest boom in fintech approaches ensuring equality of credit opportunities while pushing the envelope on the latest in advertising, underwriting and servicing.

Sources:

The fight against financial advertisers using Facebook for digital redlining

Facebook Settles Civil Rights Cases by Making Sweeping Changes to Its Online Ad Platform

'Mystery Shoppers' Help U.S. Regulators Fight Racial Discrimination At Banks

The Evolution of Redlining Post-Financial Crisis and Best Practices for Financial Institutions